Between drift and drive

My seven takeaways from the IMF-World Bank Annual Meetings this week

So I thought I’d share my read-out from the IMF–World Bank meetings, where this week I have to say it felt like a tale of two continents.

In one corner, the conversation was about just how we kickstart Europe out of its post-pandemic drift. In the other, it was about how to handle America’s drive - drive we can admire in tech and AI, but which, in trade and energy policy, there are some pretty big challenges. For the UK, these dynamics of drift and drive are going to create some big opportunities - as long as we grip some quite difficult reforms at home.

Let’s start with the European outlook.

1. Europe’s recovery has stalled

The bottom line is that across the continent, growth has flat-lined. The IMF Regional Outlook makes clear output has clawed back its pre-Covid level, but the momentum has waned. War, inflation, an ageing workforce, and the long scarring of the pandemic have left Europe stuck in neutral.

In much of the euro area, growth next year will struggle to reach 1 per cent. Central and Eastern Europe is stronger, but even there, the pace is slowing. The refrain I heard again and again in Washington: Europe is drifting, not driving.

2. Europe’s fiscal room has vanished

Fiscal space across the continent has evaporated. Debt ratios are high, borrowing costs are rising, and output gaps are closed. Governments can no longer spend their way to safety.

Without reform, average European debt could climb toward 130 per cent of GDP by 2040 — pushed up by defence, climate transition and ageing costs. So, as the IMF puts it, there’s a dilemma coming into focus: how do we pay for what Europe can no longer afford?

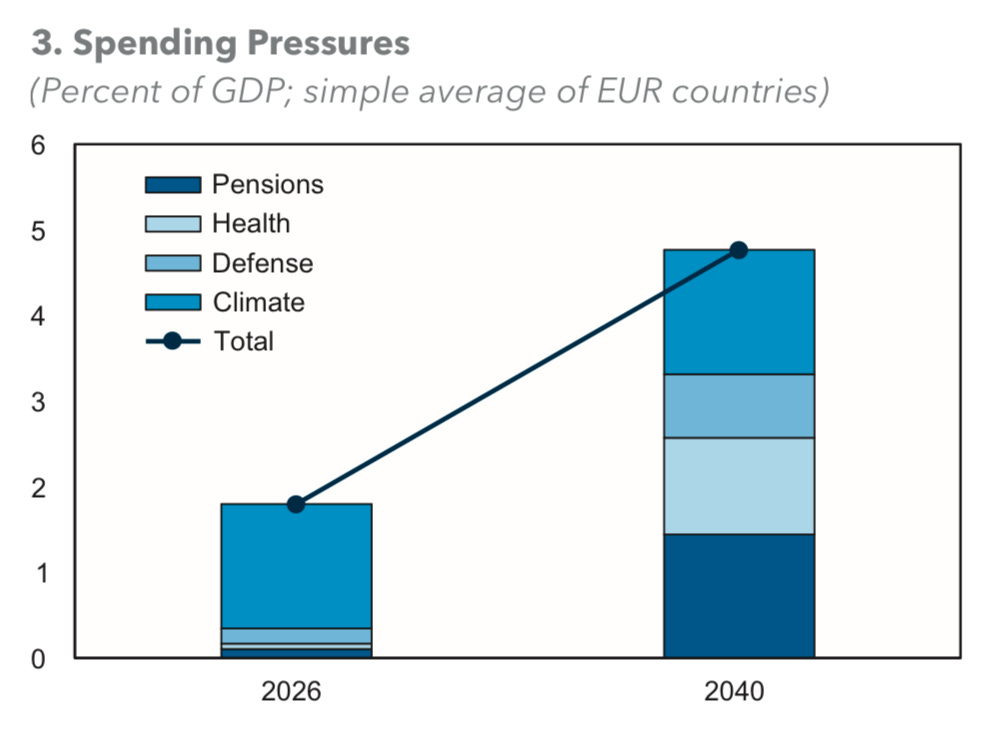

3. The squeeze: defence + climate

Defence and climate are now permanent pressures. Together they could add three points of GDP to annual spending by the end of the decade. So without faster productivity growth, that bill will be met by higher taxes or higher debt - and both choke growth.

The economists’ consensus was clear: fiscal consolidation must come with reform. And a well-sequenced package could lift European GDP by nearly 9 per cent over ten years and cut debt sharply.

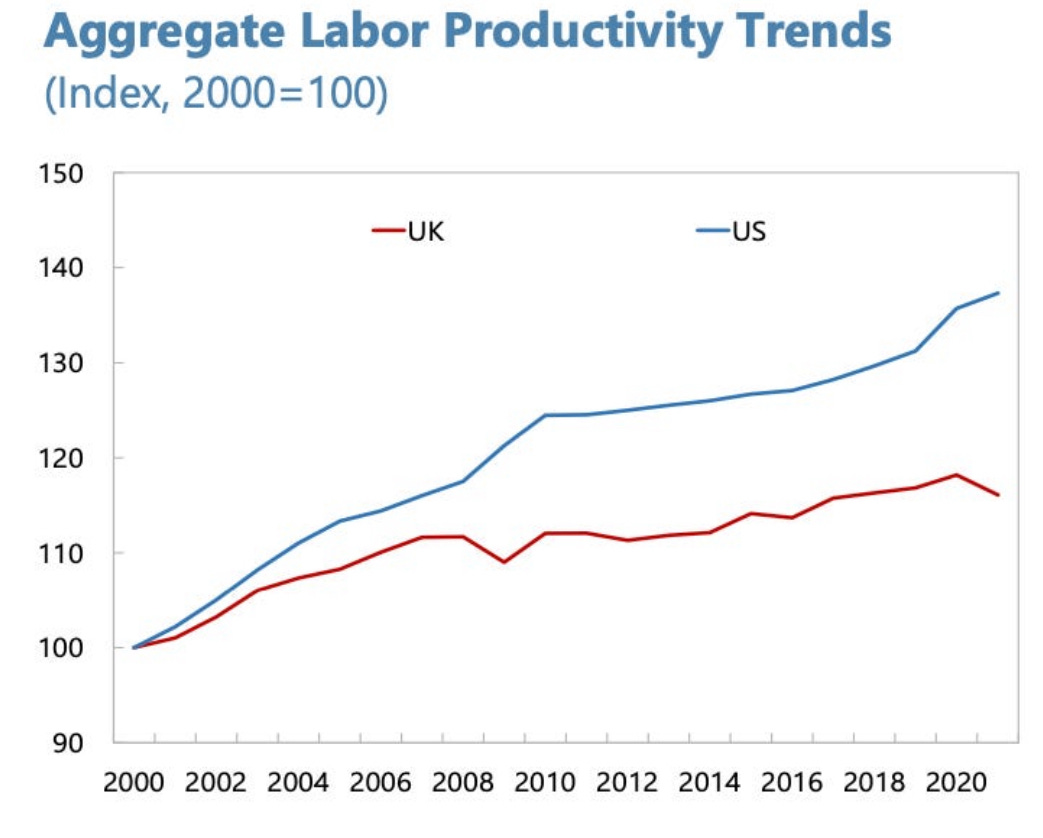

4. The productivity gap

Here lies Europe’s real weakness: productivity. Europe now produces roughly one-fifth less per worker than the United States - and the gap is widening.

This isn’t because Europeans work less. It’s because they invest less - in R&D, in venture capital, in the diffusion of innovation. Across the continent, policymakers quietly admit that Europe’s economic engine is sputtering while America’s is roaring ahead.

5. The American contrast: confidence and scale

All of this is a huge contrast to the mood in Washington about the US outlook, where the Trump Administration is shifting its statecraft forward with speed and purpose.

Officials in DC spoke with striking confidence that they have “won” the trade wars - and that tariffs, far from receding, are now embedded in fiscal strategy. Even Democrats I met - who hate tariffs - are now questioning whether, given the terrible US budget outlook, they could ever afford to do away with such a big source of income. So the question is no longer whether tariffs stay, but where they move next: perhaps into services, or towards economic-security goals.

A second shift is personnel. After months of vacancies, key figures are arriving - Jacob Helberg at State, Dan Katz at the IMF - aligned around a clear ambition to advance President Trump’s agenda through American leadership of multilateral institutions and alliances. After question marks about whether the US would leave these behind (as suggested by some chapters in Project 2025), there’s now a sense that the US will stay — and seek to lead. Hence the IMF communique was haggled through the night, with the US arguing every word and phrase. See Scott Bessant’s press notes for a sense of the argument.

I heard a much sharper intellectual coherence to this economic narrative. The administration is framing AI as the defining industrial revolution of the 21st century — a transformation that will reorder global wealth and productivity, in a way we saw during the first Industrial Revolution, from which Britain emerged as a world leader.

The argument is simple. Nations that master AI will surge ahead; those that lag will fall behind, and we should be relaxed about the labour market impact because AI adoption is correlated not with mass layoffs but with higher output per worker.

To sustain leadership, the US is now pursuing three key pillars:

• R&D: US private investment already near 3.6 % of GDP — far above Europe’s 2.2 % - and rising fast. Huge new investment in AI infrastructure from US tech firms is driving this - but I suspect tariffs are now also forcing some global capital reallocation to the US, which is going to improve US foreign direct investment numbers.

• Energy expansion: an “all-of-the-above” expansion of new nuclear, fossil fuels, new production, and new grid capacity to power electricity-heavy infrastructure like data-centres, AI and reshored manufacturing. Cheap energy is now very clearly targeted as a defining competitive advantage to master.

• Allied strategy: allies are encouraged to find their niche in the AI supply chain — in critical minerals, semiconductors, logistics or data processing — as part of a democratic growth network. The message to partners is clear: America seeks allies, not dependents, in an AI-driven world.

Be in no doubt this is going to create challenges for the UK’s China posture soon. The rare-earth row between the US and China has thrown into sharp relief what American policymakers see as the need to accelerate decoupling from China, and Mr Helberg has a reputation as among the more hawkish on China policy.

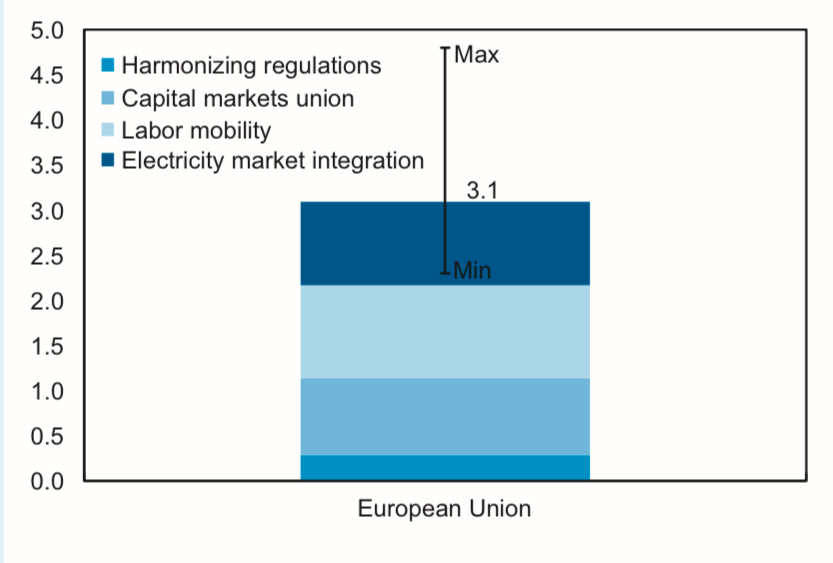

6. Europe’s internal barriers

By contrast, Europe remains tangled in its own web. Regulatory and fiscal barriers between EU markets act like hidden tariffs — 20–40 per cent on goods, more than 100 per cent on services.

Yet completing the capital-markets and services unions could add 0.3–0.4 points to annual growth — the difference between stagnation and renewal. And yet, from the Draghi plan to Lette to the IMF, there is no shortage of ideas. But there is a missing political will to turn ideas into action.

Integration is Europe’s untapped stimulus. And having spent some time with Ireland’s finance minister Paschal Donohoe, now president of the Eurogroup, I have a renewed confidence that under the Irish EU presidency some real progress is going to be made on this front.

7. The UK conversation: lessons from both sides

Get it right and the UK stands to gain a lot both from an end to European drift and from rising American drive. But there are some things we’ve got to fix.

There’s real admiration for Rachel Reeves’s determination to drive through fiscal stabilisation after the disaster of the Tory years.

But our current tempo of what is effectively two fiscal events a year is not helping - and nor is our unusual fixation with projections of fiscal headroom.

Markets reward predictability: one Budget, perhaps a twice-yearly assessment (of which one needs to be more high level), and no headline-driven tinkering. The UK / OBR obsession with five-year “headroom” is misplaced. Projections of headroom are no longer assuaging risk - they’re becoming a Westminster parlour game that unsettles, not reassures, bond markets.

To compound the problem, the design of our fiscal rules, with fixed five-year horizons for balancing the deficit, eliminates flexibility that might actually be needed to adapt to economic circumstances and risks crowding out public investment. They should be redesigned - not now, because bond markets, for a host of reasons (France, US budget gridlock), are jittery - but at some point soon.

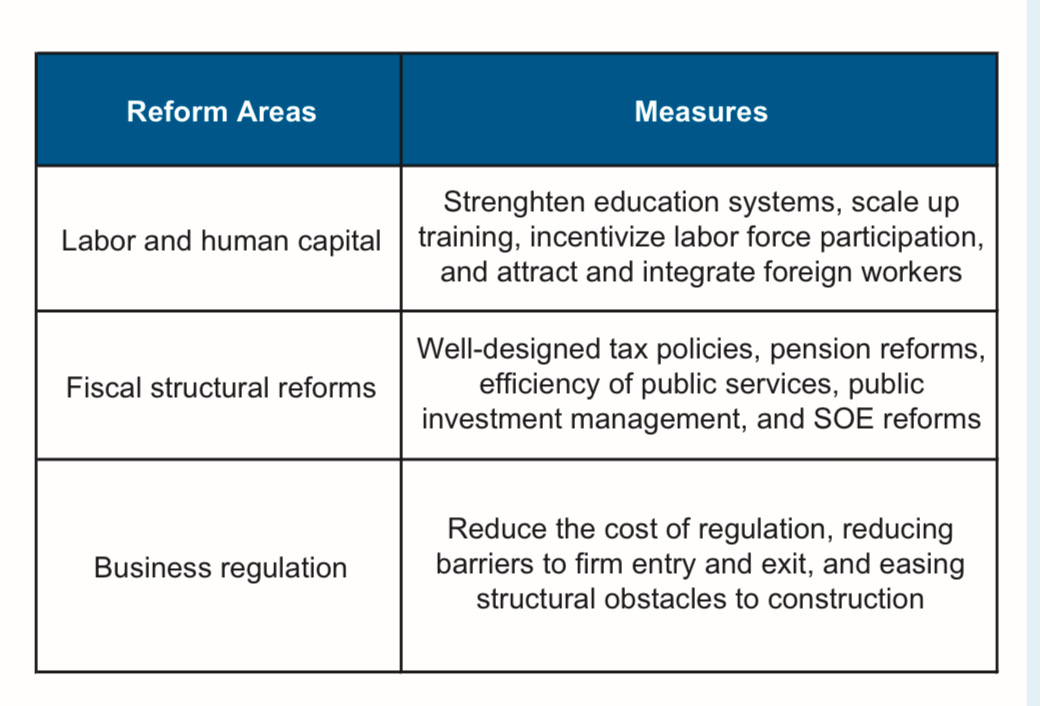

Above all, what Britain needs now is a clearer, sharper structural-reform story, perhaps focused on four or five core ideas that centre on fixing the core problem of the British economy: low investment levels and poor productivity growth.

The Treasury’s new growth model has many virtues. But it’s complicated and without much sense of a roadmap: what step follows what? How do we, as the Chinese say, cross the river stone by stone?

Based on what I’ve heard over the last few months, and the last week, here’s my view of the basic story might need to be simplified to:

Fiscal stability and public investment - the rock on which all else is built.

Double down on free trade / EU reset / global deals - this is going quite well, but the EU reset needs to go much faster.

Unblock planning and accelerate infrastructure - but, critically, bring down energy costs.

Modernise the skills system - still very much a work in progress.

Transform access to risk finance through a combination of consolidated pension funds, fixing stalled equity markets (this will need tax changes), radically expanding venture capital, expanded public-private investment institutions like the British Business Bank / National Wealth Fund - all coupled with modernisation of tax incentives for business to invest (especially in intangible investment).

Others would add regulatory simplification - though here business needs to be much clearer about the specifics of what’s problematic.

On pensions, the caution was clear - consolidate for capability, yes, but don’t compel funds into risky home assets until Britain is more investable; don’t make investors captive.

And on innovation, diffusion matters more than headlines. Productivity will rise when the next generation of technologies reaches the factory floor, not just the press release.

In conclusion…

Europe doesn’t lack ideas. America, for all its volatility, has rediscovered its drive - a strategy built on R&D, energy, skills, and allies. The challenge for Europe is to match that sense of mission. If Europe aligns fiscal discipline with competitiveness and defence, it can turn policy drift into renewal.

Britain doesn’t lack ambition. But we may lack a bit of focus. If Britain continues to stabilise its fiscal framework, rebuilds its skills base and makes capital want to come home, we can ignite a faster pace of growth. If we move with purpose, energy, focus, clarity - we stand to gain a huge prize from the years ahead, positioned as we are between our neighbours across the Channel and the wide Atlantic.

#Europe #IMF #US #EconomicSecurity #Productivity #Competitiveness #FiscalPolicy #AI #Growth #RadicalCentre

But surely Liam you are leaving too much out here. The US economy is subject to massive permanent budgetary stimulus - 6.3% for 2024 with 5.9% predicted this year amounting to $1.78tn. Accepting that EU budget rules are frequently broken, EU governments are still supposed to keep their deficits under 3%. Britain's deficit at less than 5% is considered a significant problem. The US is sustaining this only because of its reserve currency status. Whilst US growth numbers top the G7, hardly anyone would rather live in the US because US economic success is not delivering for a large chunk of its population - hence its slide into fascism. Moreover US trade and security policy is trashing US relationships with its allies and detabilising the global economy. Europeans mostly look on what is happening in the US with horror. I am sure you are right that the EU and Britain can do a lot to function better, but a reheated Thatcherism of looking to America is no way to inspire change.

Wonderfully clear and succinct. Thank you 👍