Build, don’t beg

It's America's birthday. Today, our new report on UK-US trade has some advice for how the new Prime Minister might handle the White House

Happy birthday America. Two hundred and fifty years on, there is no other economic relationship with a single country that matters more to Britain. The transatlantic market now accounts for nearly one pound of every five we earn in trade. We have £1.2 trillion invested in each other’s future. Over a million people in Britain go to work for American firms.

But this special relationship is no longer a predicable partnership. The lesson for Britain’s next prime minister is simple: build don’t beg. Don’t exhaust yourself haggling for new deals in Washington. Focus on sorting out a better business environment here at home.

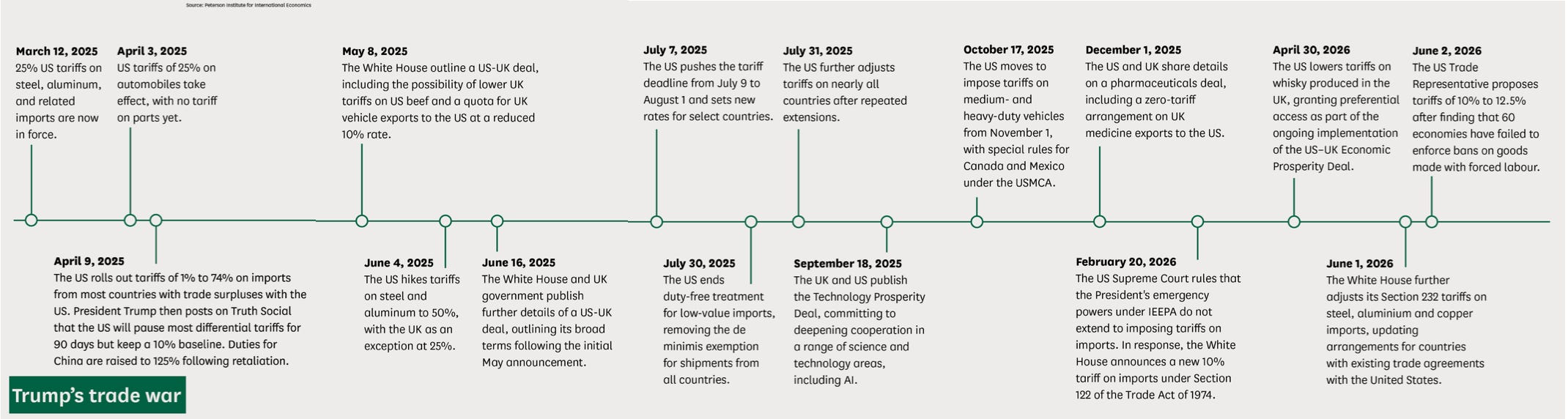

The last two years have been a rollercoaster for UK plc. Endless waves of tariffs. A new legal basis every few months. Now, President Trump is proposing yet more punitive tariffs on countries maintaining digital services taxes.

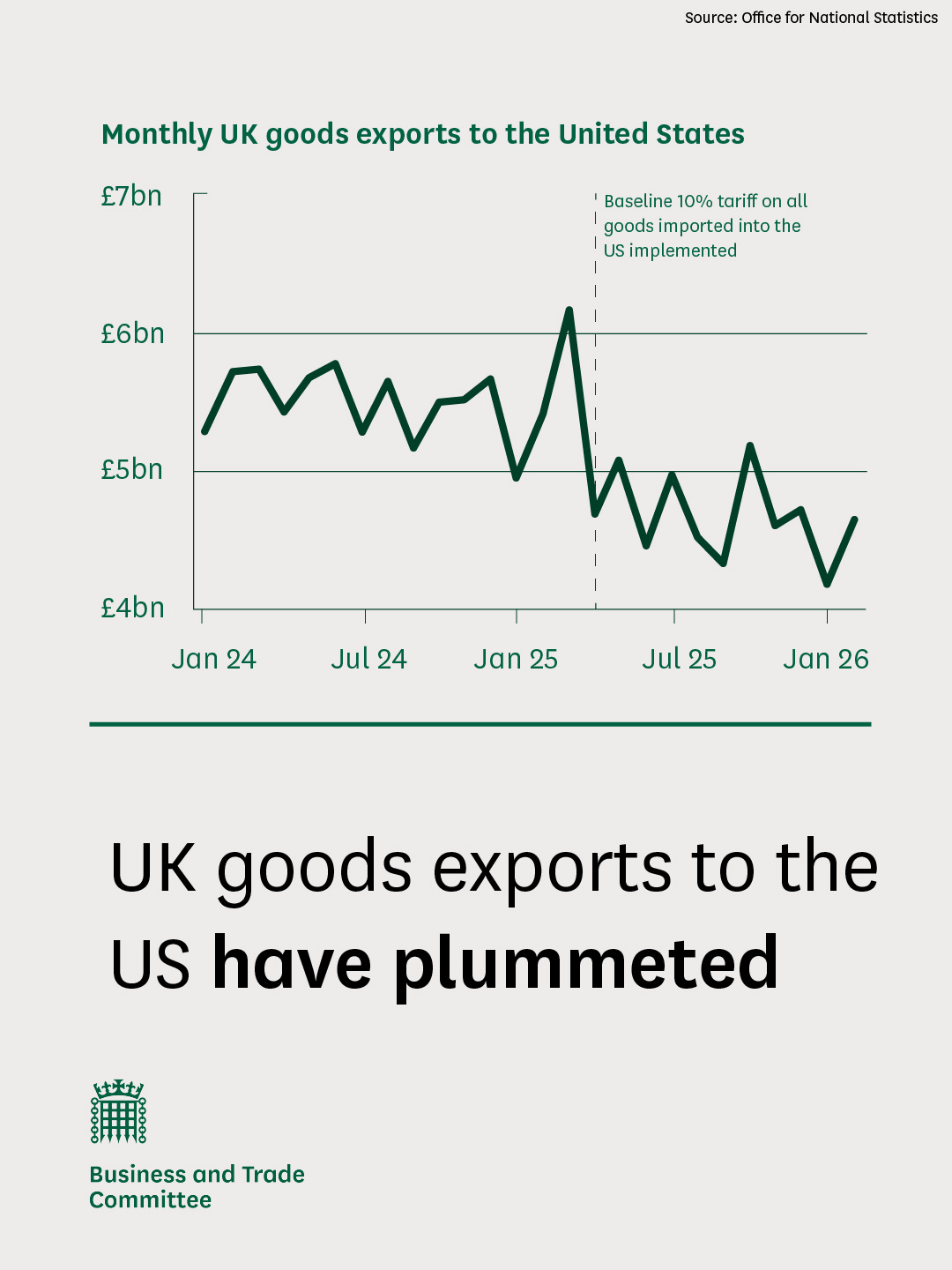

To be fair to ministers, Britain has ridden the rollercoaster better than most. Agreements covering cars, steel, civil aerospace, pharmaceuticals, lumber, whisky have all helped. Our tariff rates sit below those faced by the European Union or Japan. But we have taken a hit. While the services trade has continued to grow the goods trade is down 2.5%. We trade with our largest commercial partner on worse terms than before and the new uncertainties hurt smaller firms the most.

Yet few of our allies expect this situation to change after either the mid-terms or the next presidential election. So the lesson for the next Prime Minister, when he takes the keys of Downing Street, is uncomfortable but unavoidable. Britain cannot negotiate away an age of geopolitical insecurity.

So we must accelerate the job on diversifying our markets, draw closer to the EU, and above become the world’s indispensable place to do business.

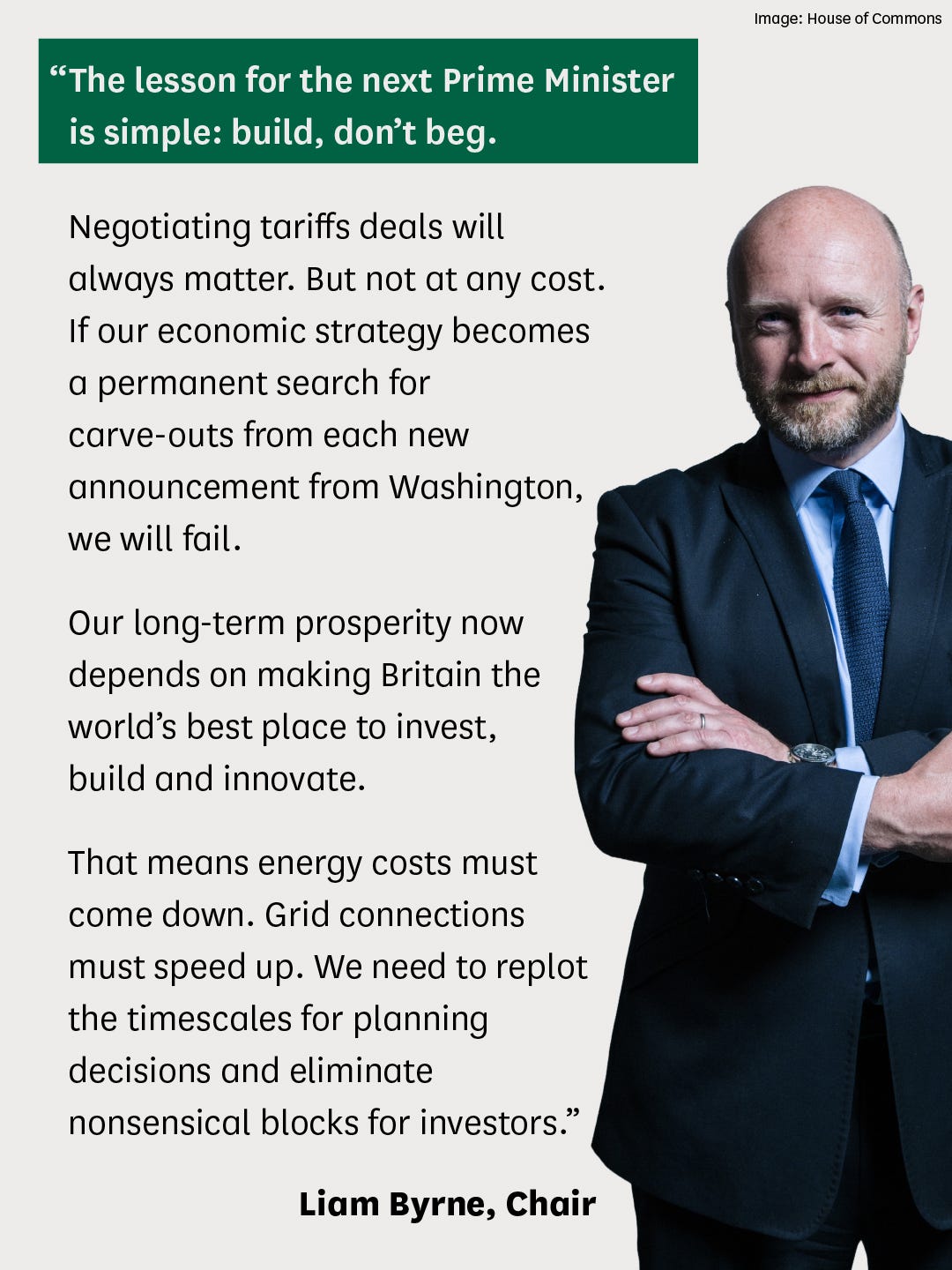

Negotiating tariffs deals will always matter. But not at any cost. If our economic strategy becomes a permanent search for carve-outs from each new announcement from Washington, we will fail.

The better strategy is to become the most attractive place in the developed world to build, invent and invest. That isn’t a politician’s slogan. It is the verdict of American investors themselves.

Look no further than the proposed Technology Prosperity Deal. It promises up to £150 billion of additional US investment - almost a quarter of the American investment stock already in Britain. Yet despite the suspension of the agreement, major investors told us they will invest regardless.

Firms like Blackstone, Microsoft and CoreWeave all make essentially the same point. They were investing not because of a deal on paper but because Britain still offers the rule of law, deep capital markets, world-class universities, a highly skilled workforce and a unique position between North America and Europe.

Nor are they asking for Britain to become the 51st state for American standards. In fact, when they are using the UK as a springboard into the wider European marketplace it can often make sense to seek a closer alignment with our closest neighbours. Becoming a passive rule-taker of US standards in areas such as digital regulation will weaken not strengthen Britain’s trusted rules for tech and jeopardise interoperability with the gigantic European marketplace next door.

As it happens US investors want to invest more not less.

But they are clear about what is stopping them.

Not American tariffs or presidential tweets - but sky-high energy costs, slow grid connections, planning delays, and a bewildering maze of institutions between boardroom approval and breaking ground. Whitehall. Local authorities. Growth zones. Combined authorities. One investor told us an electricity connection by 2029 was considered “quick”. Others described years passing before “a spade could enter the ground”. Capital is ready today. Britain often isn’t.

For thirty years Britain assumed prosperity depended on negotiating access to markets abroad.

In an age of stable globalisation, that assumption made sense. But no longer. The countries that will succeed in the next quarter century will not simply be those with the cleverest trade negotiators. They will be those with the best places to invest, innovate and build. That is the challenge facing Britain’s next Prime Minister. We should continue negotiating in our national interest. But we cannot negotiate away geopolitical uncertainty. In an age of insecurity, Britain must build, not beg.

Here’s today’s Report from the Business & Trade Committee: https://committees.parliament.uk/publications/54000/documents/301018/default/